If you’re planning to travel this fall or winter, now is the ideal time to consider purchasing travel insurance—especially if you’re a mature traveller with a complicated medical history.

Here’s why: Understanding the stability of pre-existing medical conditions is crucial when it comes to travel insurance. In today’s blog post, we will clarify what it means for a pre-existing condition to be stable in the context of TuGo® Travel Insurance. We will also cover some important definitions and provide examples to help you understand how coverage works in various situations. Let’s dive in!

Why is understanding stability important?

Understanding whether a pre-existing medical condition is stable is vital for travellers of all ages, but it is particularly crucial for seniors. It is one of three factors that can influence whether you will be covered for pre-existing medical conditions under your travel insurance policy (the other two factors being age and trip length).

What does the stability requirement for pre-existing conditions mean in travel insurance?

Stability is essential for obtaining adequate travel insurance coverage. According to TuGo’s Traveller Emergency Medical plan, a “medical condition” is deemed “stable” when the following criteria are met:

- There has been no deterioration of the medical condition, as confirmed by a physician or other licensed medical professional;

- There have been no new or worsening symptoms, nor more frequent or severe symptoms;

- There have been no changes in treatment by a physician or any alterations in medication related to the medical condition;

- No new treatments have been prescribed, recommended, or received from a physician or other medical practitioner.

For further details, read “How Unstable Pre-Existing Medical Conditions Impact Claims.”

What other key definitions are important for understanding stability?

There are three additional terms defined in our Traveller policy that are important to grasp:

- “Medical Condition”: Any disease, illness, or injury (including symptoms of undiagnosed conditions).

- “Treatment, treat, treated”: Any procedure prescribed, performed, or recommended by a physician for a medical condition. This includes, but is not limited to, medication, diagnostic testing, and surgery.

- “Alteration”: Any changes in medication usage, dosage, or type, which may include an increase, decrease, or cessation of a medication, or the addition of a new medication.

It’s important to note that “alteration” does not include any of the following:

- Switching to an equivalent brand name or generic medication of the same usage or dosage;

- Routine adjustments in the dosage of insulin or oral diabetes medication for blood level maintenance, provided the medical condition remains unchanged;

- Regular dosage adjustments of blood thinner medication to maintain correct blood levels, ensuring the medical condition remains unchanged;

- A temporary halt of blood thinner medication—up to 24 hours—if required for surgery or a medical procedure;

- Changes due to the combination of multiple medications into one, if the medical condition stays the same.

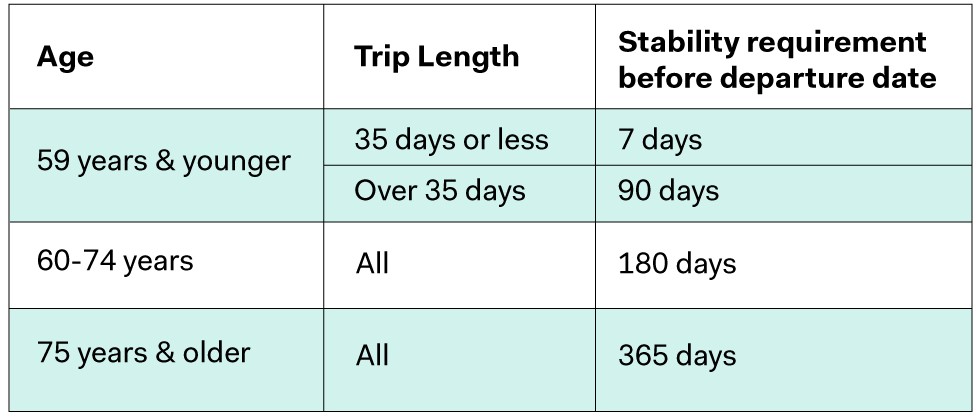

What is a stability period in travel insurance?

A stability period refers to the timeframe for which your pre-existing medical condition must remain stable before you depart for your trip.

Traveller Emergency Medical Stability Period Requirements

Note: The Travel Within Canada Emergency Medical plan does not have a stability requirement for pre-existing medical conditions.

What exclusions should you be aware of?

As with any insurance policy, there are specific terms, conditions, and exclusions you must review. Always take the time to read the policy thoroughly and address any questions or concerns with insurance providers prior to making a purchase.

Traveller Emergency Medical Insurance Exclusions

The same applies to our Traveller Emergency Medical Insurance policy. You should be mindful of all exclusions; however, there are some particular exclusions that are crucial to highlight. This will help you understand whether they might relate to your medical circumstances, prompting further discussion with your insurance professional and/or provider.

Exclusion 1: Any complications arising after the date of departure that are related to a pre-existing medical condition that was not stable before departure.

Exclusion 9: Medical conditions or related conditions for which tests to evaluate the effectiveness of a procedure, surgery, or hospitalization were scheduled or recommended prior to departure but not completed before departure.

Exclusion 10: Medical conditions or related conditions for which medical procedures, surgeries, or referrals to specialists were scheduled or recommended but not completed prior to departure.

Exclusion 14: Any medical condition for which you are on a waiting list in Canada for treatment or diagnosis.

Pre-existing medical conditions — How TuGo covered $80,000 for a senior snowbird

Meet Sophia, a 90-year-old snowbird who spends her winters in Arizona. Shortly after arriving, she developed a persistent cough accompanied by increasing shortness of breath, prompting her to seek immediate medical attention. Hospitalized for ten days due to an exacerbation of her chronic obstructive pulmonary disease (COPD), she received oxygen therapy to assist her breathing.

A year before her journey, Sophia faced health challenges related to her COPD and high blood pressure, which required two prior hospital admissions due to flare-ups. Importantly, a routine check-up with her physician just a month before her trip did not alter her treatment plan.

Since Sophia’s earlier health issues occurred over 365 days before her trip, her pre-existing medical condition was deemed stable. The recent check-up did not influence its stability because there was no change in her treatment, no new symptoms, and no deterioration of her condition. By fully disclosing her COPD history during her policy application, she successfully claimed coverage, saving $80,000 in medical costs.

Understanding your travel insurance policy is crucial before you embark on your trip. If this blog post raised additional questions, we recommend reaching out to your insurance professional or contacting TuGo’s Customer Service.

Happy travels,

Melissa

Editor’s Note: This post was originally published in August 2022 and has been updated for clarity and accuracy.

{kind=link}